Down Commodities Benefits CTA Funds

The past year has been a painful one for some macro hedge funds that focus on commodities. Recent news of the departure of the co-founders from Carlyle’s suffering commodities hedge fund manager Vermillion Asset Management, and commodities fund closures by Black River Asset Management and Armajaro Asset Management paint a grim picture of the ability […]

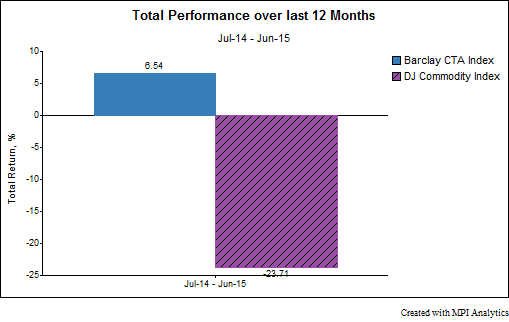

The past year has been a painful one for some macro hedge funds that focus on commodities. Recent news of the departure of the co-founders from Carlyle’s suffering commodities hedge fund manager Vermillion Asset Management, and commodities fund closures by Black River Asset Management and Armajaro Asset Management paint a grim picture of the ability of hedge fund managers to navigate recent challenging macro conditions for the sector.

Sign in or register to get full access to all MPI research, comment on posts and read other community member commentary.

Trusted by