Have Endowments Adopted The Yale Model?

We look at the largest endowments and find striking similarities in their asset class exposures. At the same time, some endowments stand out both in terms of allocations and FY2016 performance.

Using MPI’s Common Style to Understand the Endowment Landscape

Dispersion of 2016FY Results

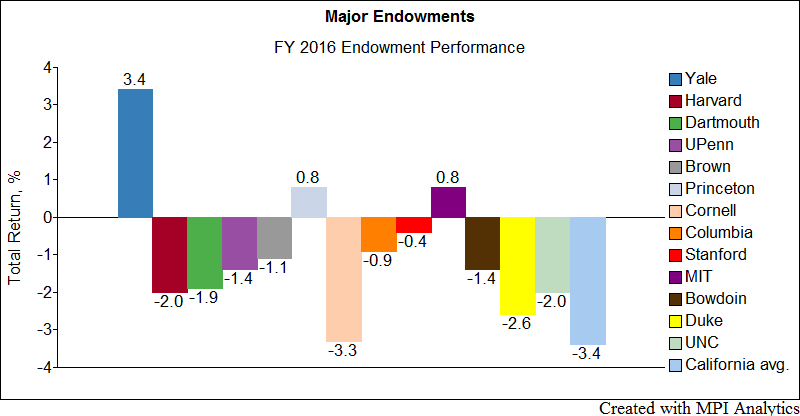

With limited data and only general information about their actual allocations, it can be difficult to identify the causes of the wide dispersion in the returns of endowments in 2016. Note the large spread between the highest and lowest performing endowments in FY2016 in the chart below (we added some additional schools to our previous analysis):

Sign in or register to get full access to all MPI research, comment on posts and read other community member commentary.

Trusted by