Ivy League Endowments Fail to Make the Grade in Fiscal 2019

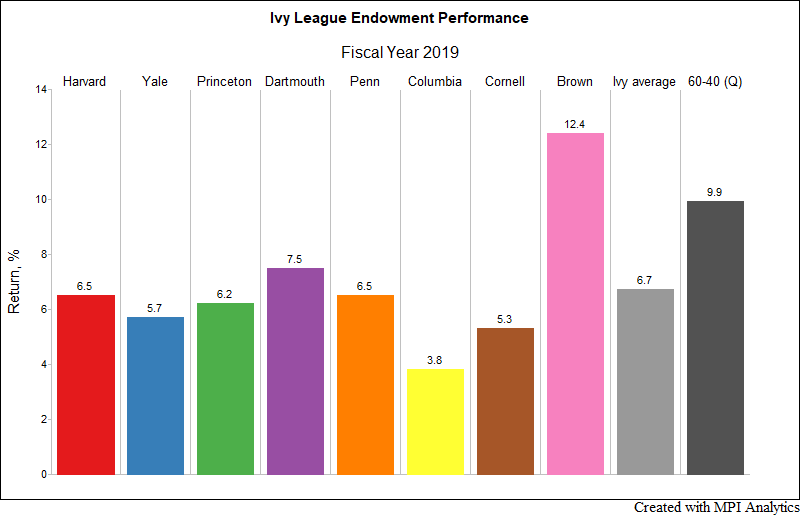

The grades for all the Ivy League endowments are in – and they are rather disappointing. Save for Brown, all Ivies underperformed the 9.9% return of a domestic 60-40 portfolio in fiscal year 2019. The Ivy average in FY 2019 was 6.7%, significantly underperforming the 60-40 and reversing two years in which they outperformed the traditional domestic benchmark.

With Princeton reporting fiscal year 2019 performance on Friday (6.2%), the grades for all the Ivy League endowments are in – and they are rather disappointing. Save for Brown, all Ivies underperformed the 9.9% return of a domestic 60-40 portfolio[1] in fiscal year 2019 (FY2019)[2]

With Princeton reporting fiscal year 2019 performance on Friday (6.2%), the grades for all the Ivy League endowments are in – and they are rather disappointing. Save for Brown, all Ivies underperformed the 9.9% return of a domestic 60-40 portfolio[1] in fiscal year 2019 (FY2019)[2]

The Ivy average in FY 2019 was 6.7%, significantly underperforming the 60-40 and reversing two years in which they outperformed the traditional domestic benchmark (see our reports for FY2018; and FY2017). In fact, this (underperformance) happened only five times over the past 16 years:

Sign in or register to get full access to all MPI research, comment on posts and read other community member commentary.

Trusted by