This white paper looks at the period of the increased volatility in the financial markets leading up to and on November 8th and provides valuable insights into internal workings of risk parity strategies during periods of heightened volatility.

This white paper looks at the period of the increased volatility in the financial markets leading up to and on November 8th and provides valuable insights into internal workings of risk parity strategies during periods of heightened volatility.

We illustrate how such an event such as “Brexit” could be (a) used as a litmus test to reconcile TDF information with performance results; and (b) alert to suitability of the selected investment option.

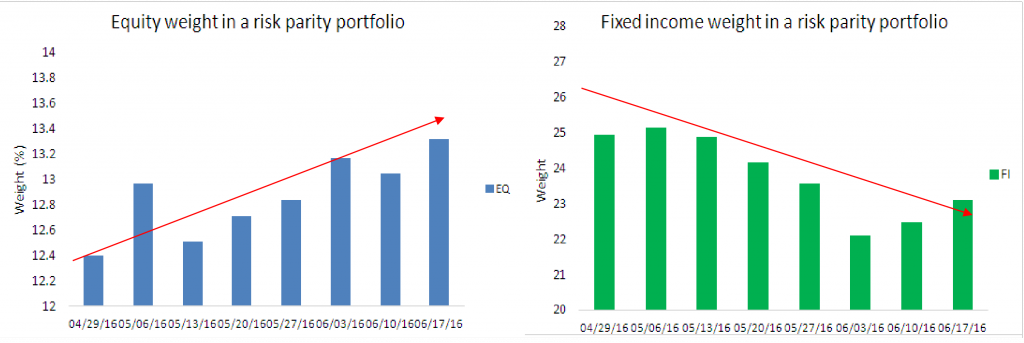

Risk parity strategies hold the promise of smooth sailing through periods of market turbulence, offering consistent performance via risk diversification. However, during Brexit the losses they experienced were very high by historical standards as they came very close to exceeding, or exceeded, the 95% worst outcome as estimated by the historical VaR.

In the world bond fund category, a dramatic change has happened: last year’s worst-performing funds are this year’s best-performing ones.