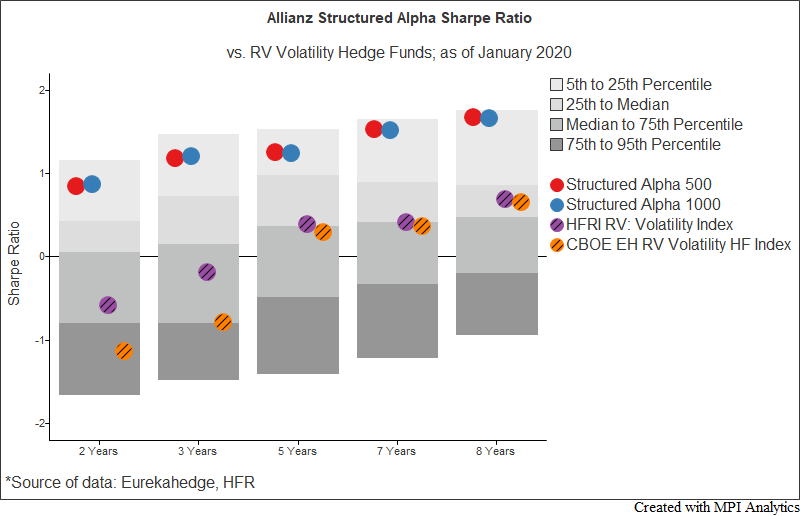

We argue that Sharpe Ratios could be hugely deceiving for derivative strategies – especially if they are in an outlier category as it was the case for the Allianz Structured Alpha funds.

We argue that Sharpe Ratios could be hugely deceiving for derivative strategies – especially if they are in an outlier category as it was the case for the Allianz Structured Alpha funds.

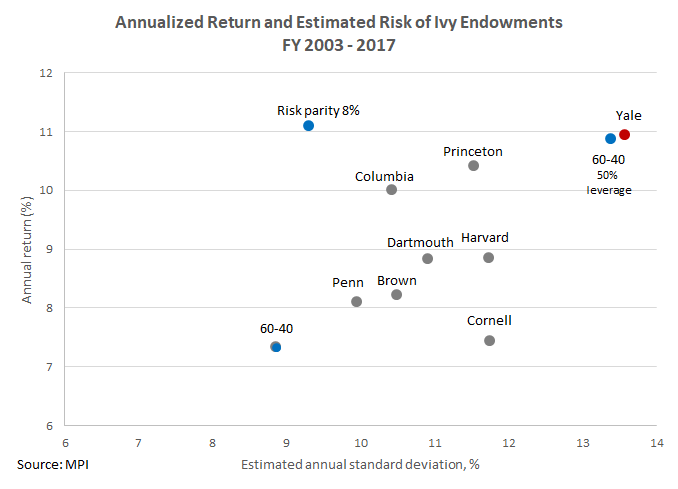

2017 Yale endowment report rebuts Warren Buffett’s 2016 Berkshire Hathaway investor letter that “financial ‘elites’”, including endowments, are better off investing in low fee index products and not “wasting” money on active managers’ hefty fees. We did our own calculations and here’s what we found…

This white paper looks at the period of the increased volatility in the financial markets leading up to and on November 8th and provides valuable insights into internal workings of risk parity strategies during periods of heightened volatility.