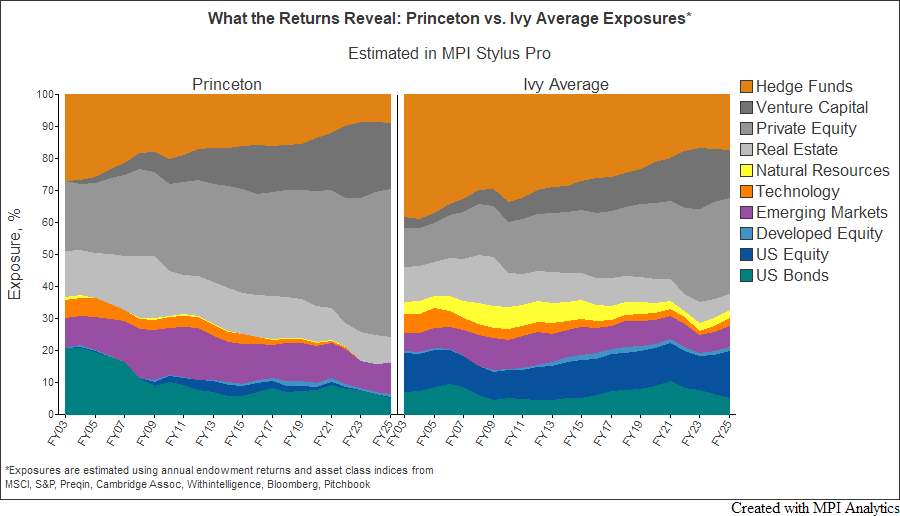

Princeton’s experience shows how hedges and changing exposures can reshape an alternative-heavy portfolio. MPI’s returns-based analysis highlights why asset owners need to look beyond allocation labels to total-portfolio behavior.

Princeton’s experience shows how hedges and changing exposures can reshape an alternative-heavy portfolio. MPI’s returns-based analysis highlights why asset owners need to look beyond allocation labels to total-portfolio behavior.

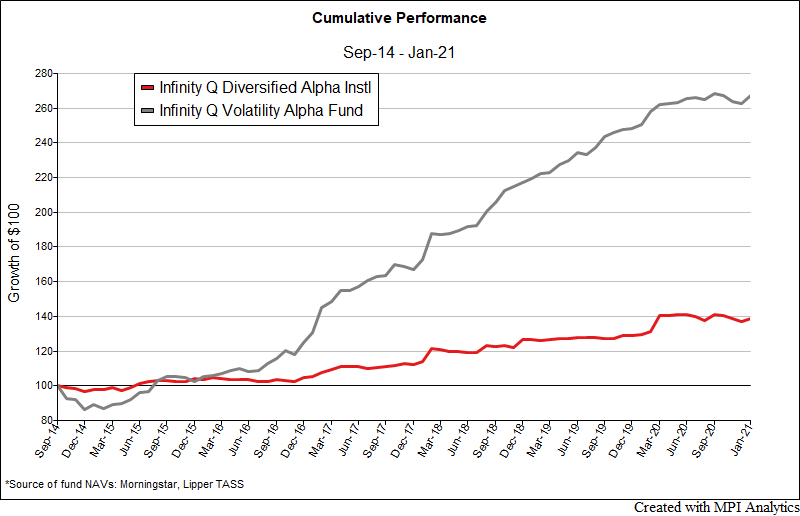

Following up on our most recent article, “Infinity Q: Too Much Alpha,” Infinity Q also managed a hedge fund product, Infinity Q Volatility Alpha, which exclusively employed volatility strategies. Using known sub-strategies as regression factors for a multi-strategy product can prove very useful in identifying the source of both skill and risk in a more complex product.

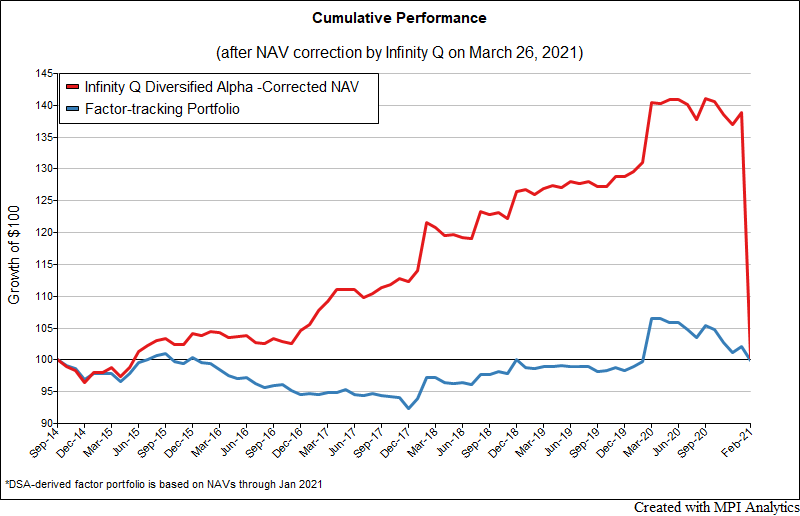

The suspension of redemptions and planned liquidation of the Infinity Q Diversified Alpha fund (IQDNX, IQDAX) – a $1.8 billion hedge fund-like multi-strategy liquid alternatives mutual fund that was started by investment staff from the family office of a private equity titan – has sent shockwaves through the fund management industry. Using MPI’s quantitative surveillance framework we discover a slew of red flags that could have alerted the fund’s investors.