MPI: Venture Capital, Technology Investments Will Define 2023 University Endowment Returns

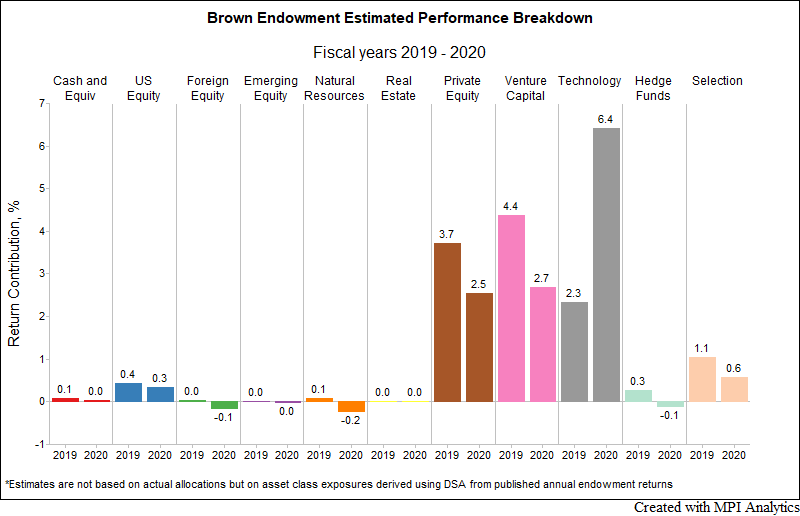

Matt Toledo with CIO Magazine reviews in this article recent performance of top endowments from Yale, UPenn and Stanford and compares them with projections from MPI Transparency Lab. “Stanford announced on Thursday a 4.4% return in fiscal 2023, slightly below MPI’s estimate of 6.42%. Stanford attributed its underperformance—as compared with Cambridge Associates’ 6.9% median return for university endowments—to losses in its venture capital investments, in line with MPI’s projections,” – he writes.